Published: November 2023

What are the advantages of using cashflow modelling in financial planning?

Cashflow modelling helps people with all kinds of different goals to find out what their finances could look like and whether they will have enough money in the future. It can help answer questions such as:

- Will I have enough money to stop working when I want to?

- How much more money do I need to save, or how much more can I afford to spend?

- Can I afford to reduce my working hours leading up to retirement?

- How much investment risk do I need to take to achieve my goals? Can I afford to reduce or even increase my exposure to investment risk?

- If investment markets fell suddenly, how would this impact my retirement plans?

- How do my savings, such as ISAs, pensions, shares, property, and business assets, contribute to my overall retirement income?

- How can I take an income in the most tax-efficient way possible?

- Would my family be sufficiently provided for in the event of my premature death?

- Will my family be financially stable if I go into care?

- Am I going to leave behind an Inheritance Tax (IHT) bill?

- Can I afford to make gifts to my loved ones e.g., house deposits?

At MM Wealth, we consider various scenarios to determine their impact on your finances. This enables us to offer more informed advice on achieving your lifetime goals.

How can a chartered financial planner help you?

The first step is to discuss detailed information about your current finances.

- How much income do you receive each month?

- What are your outgoings?

- How much money have you [and your partner] saved in pensions, ISAs and other investment and non-investment accounts?

- Are you expecting to receive a future inheritance, sell a second property, or downsize from your main residence at some point in the future?

Our cashflow modelling programme creates a long-term projection of your finances using the data you provide, along with what we believe to be realistic long-term investment and economic assumptions.

Our analysis will consider all your financial resources, take into account any potential taxes you may incur, and identify any surpluses or shortfalls.

The more information you provide about your goals and financial situation, the more accurate the projections will be.

Case study – will I have enough money in retirement?

Bob is a 58-year-old businessman who runs a business with his wife, Susan, who is also 58 years old. The couple plan to retire at age 60 but wanted to ensure they had enough funds to support their desired retirement lifestyle.

They consulted with one of our financial planners to determine if they could afford to reduce their working hours leading up to retirement and allocate more funds towards travel during the early stages of retirement. Additionally, they wanted to ensure that they could afford any future care home fees for peace of mind.

Preparing for the first meeting with their Chartered Financial Planner

Bob and Susan shared information about their financial situation prior to the meeting. e.g., details of their assets, savings, and liabilities, including pensions, investments, mortgages, and business accounts.

They also listed their expected expenses leading to and during key stages of retirement, such as pension contributions and regular expenses, as well as other planned expenses like a new car and annual holidays.

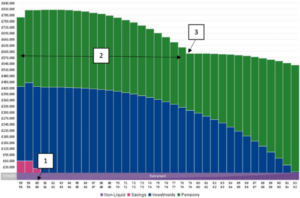

A cashflow model is prepared as per below: –

Example cashflow illustration

- Bob and Susan retire at age 60.

- The couple’s discretionary expenditure is at its highest from age 60 to age 80, as this is the period in which they envisage spending more on holidays.

- There is a reduction in expenditure at age 80 as they expect to begin spending less.

During our cashflow modelling session, Bob and Susan discovered they had saved more than enough money to achieve their desired retirement lifestyle. They had the option to retire immediately and live comfortably until they were 92, while still leaving an inheritance for their children. This revelation gave them peace of mind and allowed them to feel content with spending more during their retirement.

With the knowledge that they would be able to leave assets behind when they passed away, Bob and Susan decided to meet with their financial planner in a month’s time to discuss giving their son a cash gift to help him onto the property ladder.

Additionally, the cashflow modelling provided Bob and Susan with reassurance that they would have access to significant capital in later life to cover potential care home fees, without the need to release capital from their property.

For bespoke financial planning and investment advice, please speak to a member of our financial planning team on 01223 233331.

Disclaimer

Opinions constitute our judgment as of this date and are subject to change without warning. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment.

The information in this article is not intended as an offer or solicitation to buy or sell securities or any other investment, nor does it constitute a personal recommendation.

The information contained within this blog is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

The Financial Conduct Authority does not regulate tax planning.

{kind=link}